Correcting Vesting Errors

A Segment in Our Retirement Rescue Series

A Segment in Our Retirement Rescue Series

“Vesting” refers to the ownership a participant has in the assets that are contributed to their account by their employer. Should the participant terminate their employment, their vested percentage determines the amount they are entitled to.

Participants are always 100% vested in the money they have contributed to their account. This means they are fully entitled to their contributions and associated earnings upon a distributable event, such as termination.

Vesting for contributions made to a participant’s account by the employer, such as matching and profit-sharing contributions, is determined by the Plan’s vesting schedule.

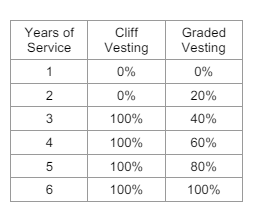

Plans often use one of the following IRS-approved minimum schedules:

The chart below compares cliff vesting and graded vesting:

Plans may use more generous schedules (e.g., immediate vesting), but they may not be less favorable than these statutory minimums.

Additionally, a participant is automatically 100% vested upon reaching normal retirement age or if the plan is terminated. Many plans also fully vest participants upon death or disability, though this is not a requirement.

Since vesting is based on Years of Service as defined by the Plan Document, using inaccurate service records or the wrong definition of Years of Service can lead to vesting errors. Common mistakes include:

Inaccurate vesting determinations can cause participants to receive incorrect benefit amounts when they take a distribution (either too little or too much). If vesting errors are not corrected, the plan may risk losing its tax-qualified status.

The Employee Plans Compliance Resolution System (EPCRS) provides methods to correct vesting errors.

Under Rev. Proc. 2021-30, the Self-Correction Program (SCP) may be used to correct vesting errors — even if significant — as long as the plan sponsor has established compliance practices and the correction is made within three years of the Plan year in which the error occurred.

If the failure is not eligible for SCP (e.g., it’s older than three years or involves a systemic issue without compliance procedures), the error must be corrected through the Voluntary Correction Program (VCP).